- tmrw

- Posts

- Modern Risk

Modern Risk

The risks dominating the headlines right now are not always the risks sitting inside your financial life. In this edition, Tom Stadum revisits the LIVE WELL Framework to explain how modern risks pair together, why the assumptions inside most financial plans deserve an honest review, and how disciplined investors find opportunity inside disruption. If you are building toward retirement in a world defined by AI, geopolitical tension, and market volatility, this is the context you need.

Tom Stadum

April 02, 2026 • Read Time: 5 minutes

This is tmrw — a weekly note on money, decisions, and what tends to matter over time.

Modern Warfare. Modern AI. Modern Health. Modern Politics.

I wrote at the beginning of the year that defense is the best offense. Protecting your gains, tax planning, and staying nimble at the wheel are some of the best ways to operate in this environment. Here we are at the end of quarter one, beginning quarter two, and that has proven true. The throughline of 2026 has been defined by three things: tech (AI), investor psychology, and geopolitical risk.

The headlines right now are honestly brutal. Oil above $100 a barrel. The S&P 500 oscillating around correction territory. An active war. I don't think anyone predicted we'd be having this year. But here we are.

This week I want to talk about risk. Modern risk. And I want to explain it in the context of what you need to know versus what gets presented to you as you scroll through your news feed, watch TV, and go about your week. As a friendly reminder, the platforms driving the narrative, in both good ways and not, have been sued and investigated over "addictive" design features that allegedly harm young users' mental health.

Make of that what you will, but the court cases say the mediums we all use to consume information about our world are designed to be addictive, and the follow-on effects show up as a mental health issue with young people.

Put another way, the narrative shapes us. The platforms are just platforms. I have a feeling we'll look back and find that we were the problem.

But to risk. Last summer I wrote about the LIVE WELL Framework. It is a system I created to help families understand the risks they actually face in the midst of the narrative. Risk is something you innately feel. It is hard to describe and it often looks different than what is presented or shared.

Here are the risks you actually face in your financial life:

L — Longevity Risk. Living significantly longer than expected, stretching savings thinner than anticipated.

I — Inflation Risk. Inflation silently reduces purchasing power, especially in healthcare, housing, and daily living.

V — Volatility Risk. Market ups and downs, particularly at the onset of retirement, can dramatically impact portfolio longevity.

E — Estate and End-of-Life Risk. Without thoughtful planning, your assets may not reach those you intend, in the way you intend.

W — Withdrawal Risk. Withdrawing from your portfolio at the wrong time, especially during a downturn, can permanently damage your retirement.

E — Emergency and Liquidity Risk. A lack of accessible cash can force you to liquidate assets under the worst possible conditions.

L — Legislative Risk. Tax codes, retirement rules, Social Security, and estate tax laws keep changing and can meaningfully alter your plan.

L — Long-Term Healthcare Risk. Healthcare and long-term care costs remain one of the greatest financial threats in retirement.

Let's make this practical.

What you are experiencing right now is volatility risk. You open the stocks app on your phone and the market cannot seem to get a break. It feels defeating, and in the short term, it is. Market history tells us corrections happen roughly every year, and a bear market, defined as a decline of more than 20 percent, comes around every three or four years. Yet long-term equity returns have historically averaged around 10 percent per year. What you are feeling in your portfolio right now is completely normal, even though the circumstances that led to this are not.

But here is what I want you to know: you rarely face one risk at a time.

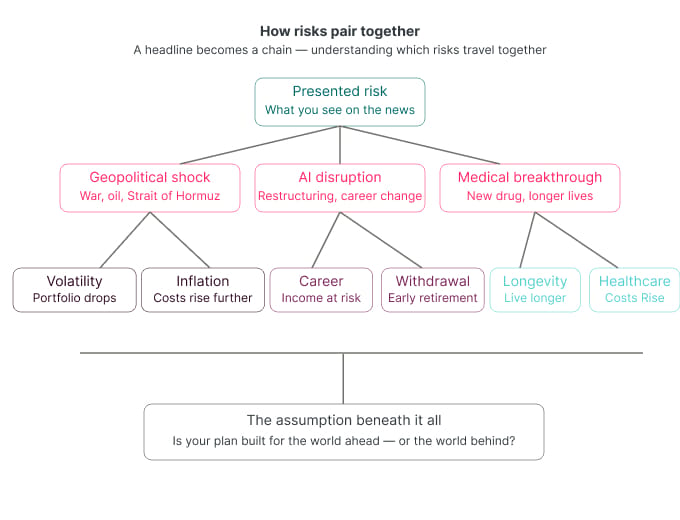

Risks pair together.

Understanding this separates the wheat from the chaff

I have spoken to many clients over the last few months who are worried about the career effects on their children and grandchildren from AI, something I explored in detail earlier this year. They see the news, talk with their kids, and we talk about it together. The overarching theme is uncertainty. It feels risky. And it is.

Here is how I frame it for them: what if they need to support their children due to an unforeseen layoff? That single event poses a liquidity risk, a tax risk, an investment risk, and a longevity risk increase, all at once. This is how risk functions in real financial plans.

The risks being presented to you on television are not the same as the risks sitting in your financial life. Geopolitical risk, the Strait of Hormuz, oil prices, get translated into market volatility, which then creates pressure on your longevity assumptions, which compounds into long-term care cost projections you never updated. The presented risk is a headline. The real risk is what that headline means for your family ten and twenty years from now.

Beneath the LIVE WELL framework lives something I, as a financial planner, am watching closely: assumptions.

The dangerous risk right now is not what the market is doing in a vacuum. It is the possibility that financial plans are not built or optimized for the world we are heading into.

Many plans since the financial crisis have flourished under low rates, career stability, US market dominance, and predictable inflation. Those were the assumptions five years ago. Today, they are legitimately in question, simultaneously. It is worth remembering that in 2016, central banks around the world were desperately trying to solve stubbornly low inflation left over from the financial crisis. Low inflation was great for asset prices. Today we are dealing with the opposite, driven by wars in the Middle East and Ukraine.

So while the environment is new, the risks remain the same.

Here is a concrete example of how to use this framework. Just yesterday, the FDA approved a new weight loss drug, Foundayo, from Eli Lilly. The stock popped.

On the surface the story is obvious. But think it through. If this drug becomes a commercial success and people are healthier and living longer, that translates directly into longevity risk. It costs money to live. Five additional years of inflation-adjusted retirement spending is a real number. At the same time, given the geopolitical turmoil creating a dip in certain stocks, a company like Eli Lilly sitting at the intersection of AI-driven drug research and a blockbuster approval might represent an opportunity worth examining in your portfolio.

The framework is not just for managing fear. It is to help you contextualize what actually matters to your financial life.

If you are 53 and work at a company going through AI-driven restructuring, the risk is not abstract. If you receive a year of severance and are not financially positioned with adequate liquidity, the pressure to cash out a portion of your 401k becomes very real. You pay the taxes. You pay the penalty. You permanently remove that money from compounding. That is the kind of mistake that follows a family for decades, and it can be avoided with the right preparation today.

Remember, risk can never be avoided, only managed.

I will be the first to admit that I have had more than a few conversations with myself this year about what AI means for our business, our clients, the markets, and the economy. The situation in the Middle East is complicated in every sense.

But it has always been this way.

It is our job to respond.

I want you to leave this week with something more useful than fear and anxiety. There is enough of that in our world.

Use the LIVE WELL framework. Map the risks actually present in your life right now, not just the ones on the news. Look at how they are pairing together. Ask honestly whether the assumptions inside your financial plan still hold. And then look for the opportunities hiding inside the disruption, because they are always there for the investor who is paying attention.

The risks are modern. So is your ability to navigate them.

Tom

If you’d like to talk through how this applies to your own financial life, you can learn more about our work at Fjell Capital here.

And if you found this edition useful, let me in the poll below or reply with a quick note—I read every response.

More next week.

How helpful was this week’s edition?Comment after you submit. Your feedback helps shape what I write in future editions. |

|  |  |